Ukraine’s Defense Tech Industry 2022–2026 - From Battlefield Innovation to Scalable Defense Ecosystem

Since Russia’s full-scale invasion in 2022, Ukraine has built one of the most dynamic and operationally driven defense technology ecosystems globally. What began as a small, volunteer‑supported and angel‑funded community has rapidly evolved into a large-scale industrial sector tightly connected to battlefield feedback, state procurement, and international defense cooperation.

Between 2022 and 2025, the number of defense tech companies grew from roughly a dozen to around 1,500. The sector experienced exceptional growth: several companies reached revenues exceeding USD 100–180 million in 2024, and long‑established firms expanded revenues more than 100× while increasing staff over 25×. This demonstrates a decisive shift from “garage-style” innovation to an industrialized defense economy. Localization has accelerated, driven by shortages of foreign components (especially from China) and urgent frontline demand.

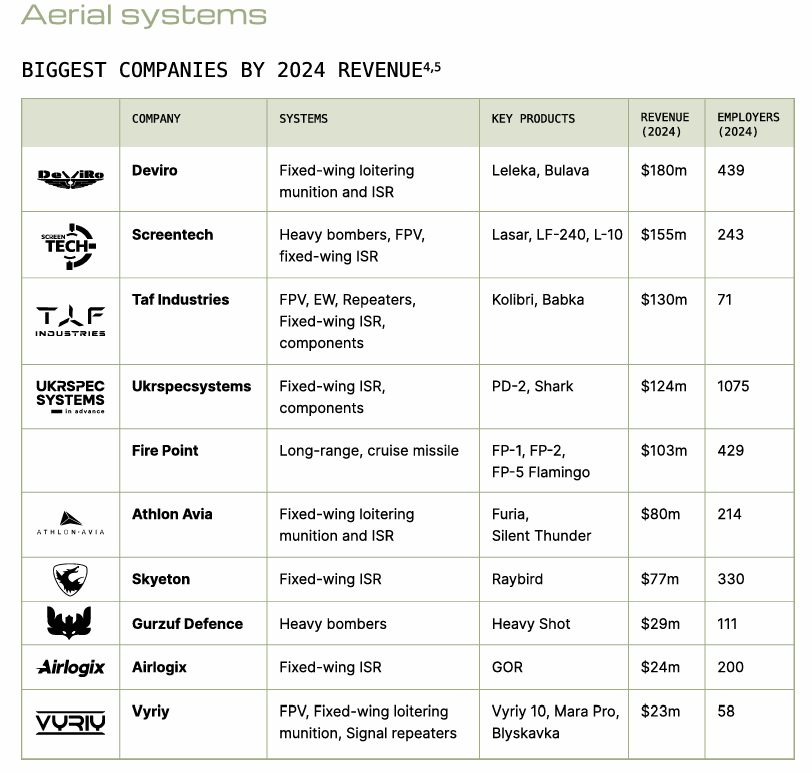

Aerial Systems (UAVs)

Aerial systems are the most developed and strategically decisive segment. Key companies include DeViro (Leleka, Bulava), Screentech (Lazar, LF‑240), TAF Industries (Kolibri, Babka), Ukrspecsystems (PD‑2, Shark), Fire Point (FP‑1, Flamingo cruise systems), Athlon Avia (Furia), Skyeton (Raybird), Gurzuf Defense, Airlogix, and Vyriy.

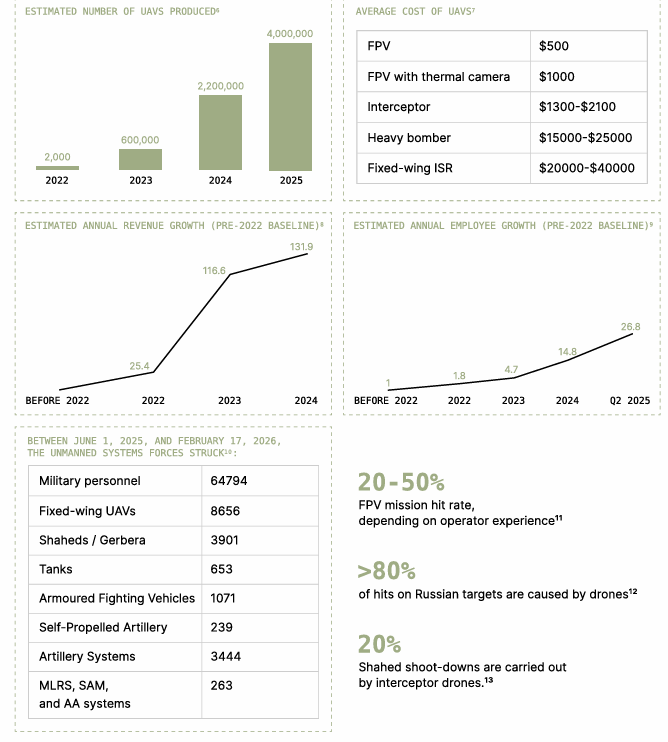

These firms cover FPV drones, loitering munitions, ISR platforms, heavy bombers, long‑range strike UAVs, and interceptor drones. Estimated UAV production rose from thousands in 2022 to millions annually by 2025, with drones responsible for over 80% of hits on Russian targets, underscoring their central battlefield role.

Ground Systems (UGVs)

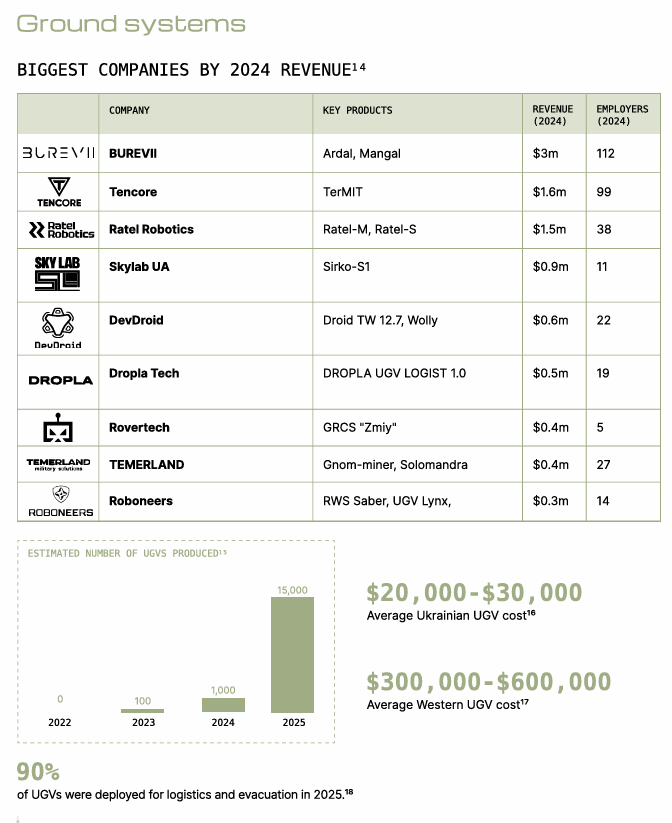

Unmanned ground vehicles are a rapidly scaling but still emerging sector. Major players include BUREVII (Ardal, Mangal), Tencore (TerMIT), Ratel Robotics (Ratel‑M/S), Skylab UA, DevDroid, Dropla Tech, Rovertech, TEMERLAND, and Roboneers. Approximately 15,000 UGVs have been produced, with 90% used for logistics and evacuation rather than direct combat. Ukrainian UGVs remain dramatically cheaper than Western equivalents, providing a cost‑effective model for mass deployment.

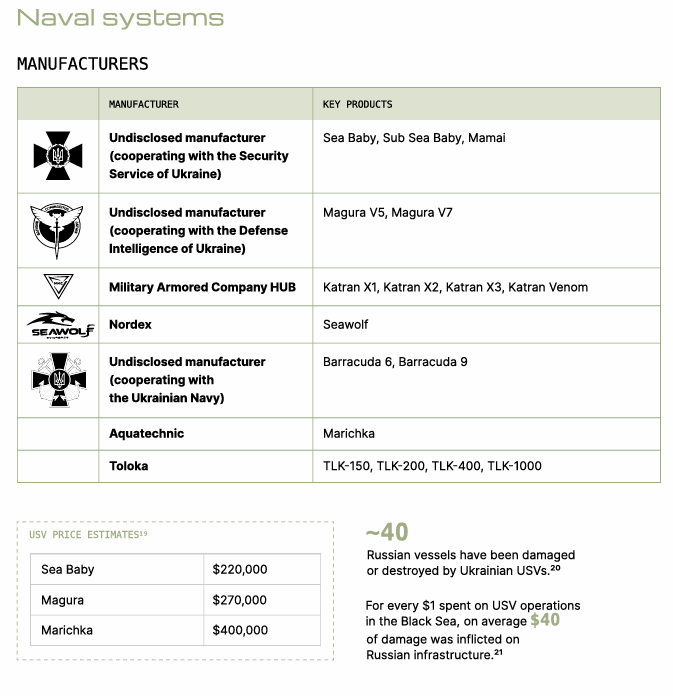

Naval Systems

Naval drones have delivered disproportionate strategic impact in the Black Sea. Systems such as Sea Baby, Magura V5/V7, Katran, Barracuda, Marichka, and Toloka—produced by a mix of disclosed and undisclosed manufacturers working with Ukrainian intelligence and naval services—have damaged or destroyed roughly 40 Russian vessels and major infrastructure targets. Their cost‑exchange ratio is extraordinary: for every USD 1 spent, Ukraine inflicts an estimated USD 40 in damage.

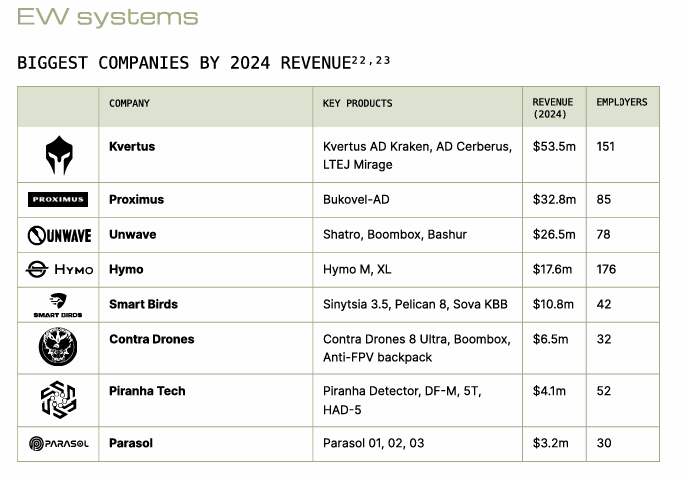

Electronic Warfare (EW)

EW represents a mature and commercially significant sector. Leading companies include Kvertus, Proximus (Bukovel‑AD), Unwave, Hymo, Smart Birds, Contra Drones, Piranha Tech, and Parasol. These firms develop anti‑drone rifles, personal and vehicle‑mounted jammers, trench-based systems, and SIGINT solutions, continuously adapting to Russian countermeasures. EW revenues rank among the highest outside the UAV segment.

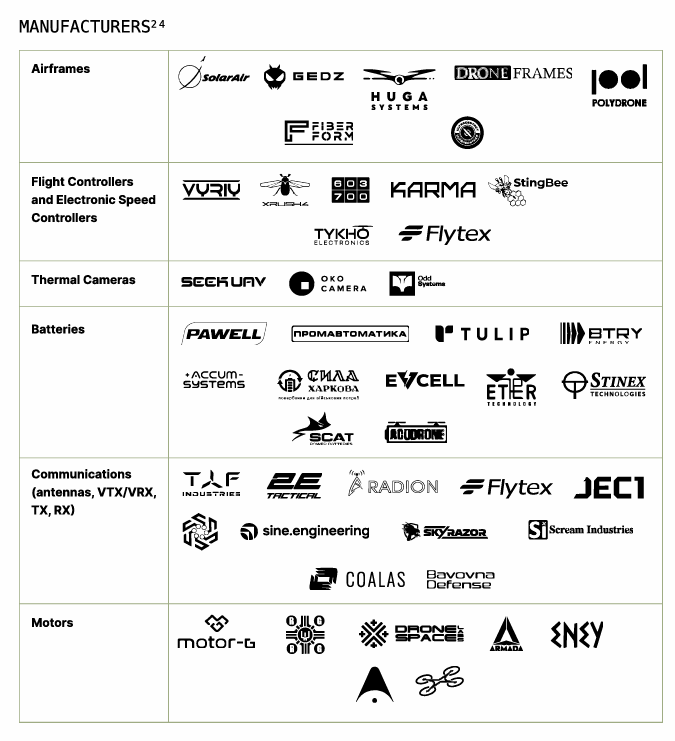

Components, Software, and AI

Localization of components is one of the fastest‑growing trends. Over 70 Ukrainian component manufacturers now produce airframes, communications equipment, motors, avionics, and thermal cameras. Companies increasingly integrate Ukrainian-made parts, with 80% of UAV manufacturers already using domestic components. Software, AI, autonomy, secure communications, and battlefield analytics are decisive enablers across all systems and attract the highest share of venture investment.

Investments and Funding

Investment evolved from predominantly angel funding in 2023 to a structured ecosystem involving venture capital (D3, Green Flag Ventures, MITS Capital, UA1 VC), strategic investors (e.g. Rheinmetall), and state and international programs. Total investment reached ~USD 129 million in 2025. Public funding expanded dramatically, with weapons procurement spending increasing sixfold since 2022, supported by agencies like Brave1, innovative digital procurement platforms, and combat reward systems.

Next Steps and Outlook

Looking forward, the report identifies AI, software, and communications as the highest-investment sectors, components as the fastest‑growing, and UGVs and components as the most promising for near‑term expansion. Continued localization, scale‑up of production capacity, and deepening international co‑production (with the EU, UK, US, and NATO partners) are expected. Ukraine’s defense tech sector is gradually transitioning from wartime survival innovation toward a sustainable, export‑capable defense industrial base, shaping future models of modern warfare and defense technology development.